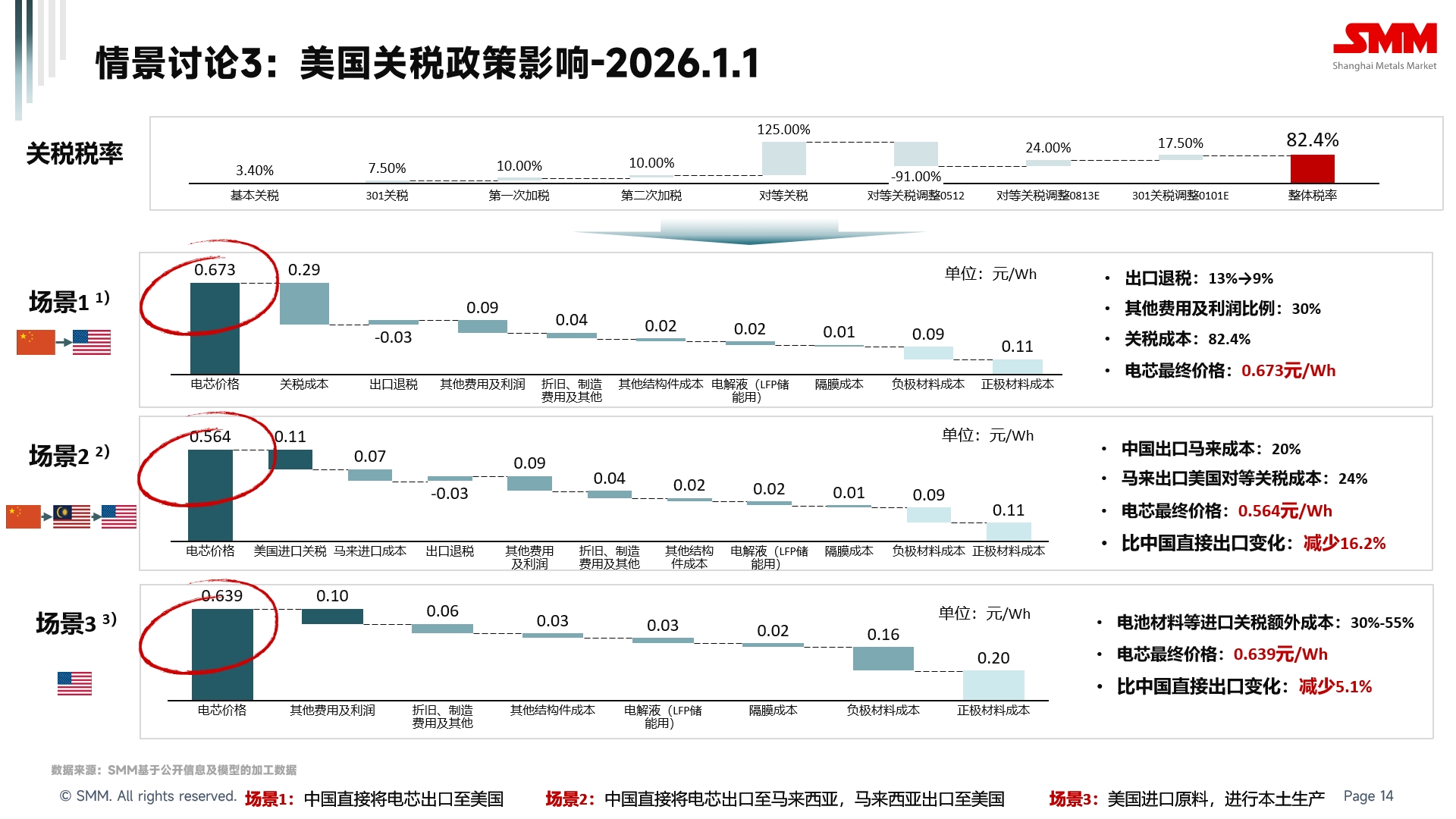

This article is the third in a series on the export methods and price impacts of China's energy storage cells to the United States under the backdrop of U.S. tariffs on China. The previous articles have mentioned that, despite the current uncertainties of U.S. tariffs on China, the existing energy storage tariff measures are divided into three time nodes: May 14, 2025, August 13, 2025, and January 1, 2026, with tariffs set at 40.9%, 64.9%, and 82.4%, respectively.

This third article aims to analyze the price impacts on energy storage cells produced in China and exported directly, re-exported via Malaysia, and those potentially manufactured in the U.S. using lithium iron phosphate (LFP) technology after January 1, 2026. Some of the data used are theoretical, which may result in seemingly high outcomes. The author will provide detailed explanations for the data values to enable readers to replace relevant data and obtain more targeted conclusions.

Taking the domestically produced 280Ah lithium iron phosphate (LFP) energy storage cell as an example:

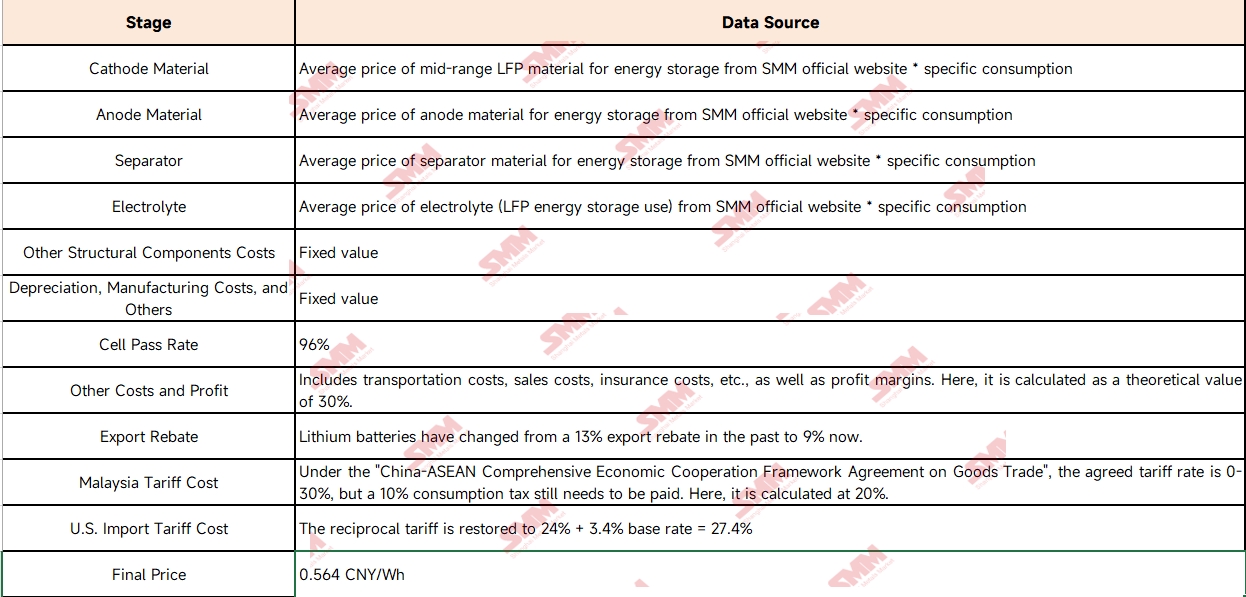

(1)The data sources and changes for each link are shown in the table below: Direct export from China to the U.S.

(2)The data sources and changes for each link are shown in the table below: Transshipment from China to the U.S. via Malaysia:

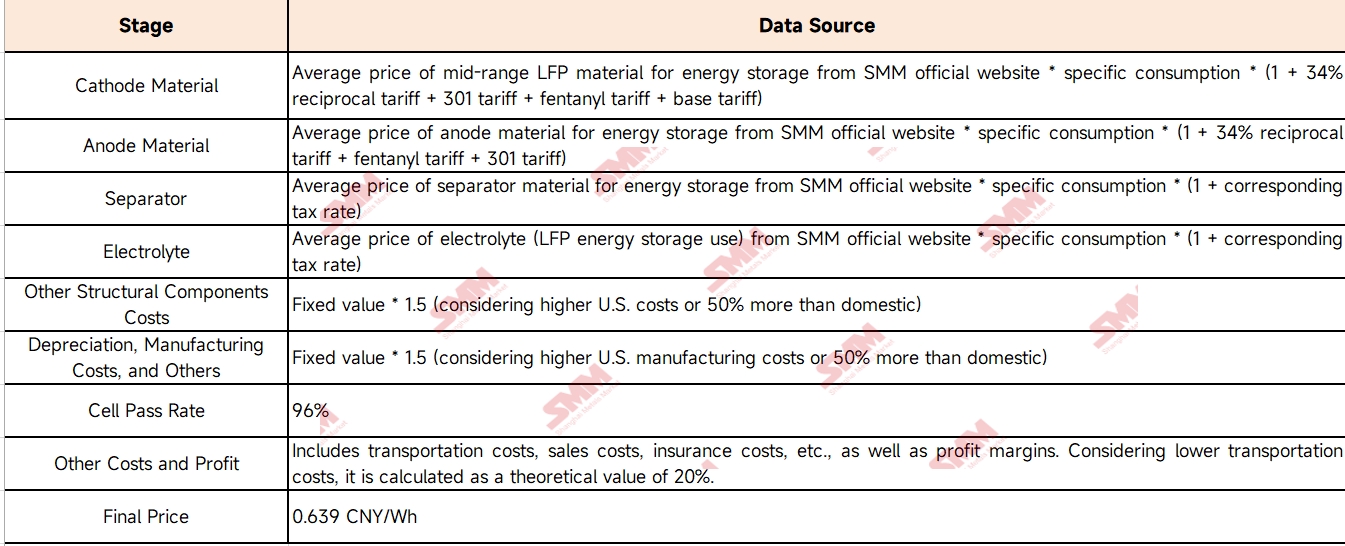

(3)The data sources and changes for each link are shown in the table below: Locally produced LFP cells in the United States:

To sum up the above calculations, after January 1, 2026, taking the direct export price of cells from China at 0.673 CNY/Wh, the transshipment via Malaysia has a price advantage of 16.2%. The cost of directly producing energy storage cells in the U.S. may also have a relatively competitive edge under the high tariffs, reducing the price by 5.1% compared to directly purchasing cells from China.

Summarizing the three articles in this series, the author believes that around 70% of U.S. tariffs on China may be a theoretical equilibrium level. If the tariffs are below around 70%, China's LFP energy storage cells still have a price advantage over those produced by the U.S. on its own production lines. If the tariffs are above around 70%, it would be more advantageous for the U.S. to produce LFP energy storage cells locally. However, assuming that the transshipment trade channel is not completely blocked, transshipment trade remains the most economical way of trade.

The above summary is organized as follows:

Note: Some of the calculated data were obtained by the author through communication and processing in the market, while more data originated from the average prices of various stages on the SMM official website. In addition, in the current actual operations, the increased costs resulting from the U.S. tariffs on China are mainly borne by overseas clients. Therefore, the results calculated in this article may be higher than the actual transaction prices. Any improper aspects are welcome to be criticized and corrected by everyone.

SMM New Energy Industry Research Department

Cong Wang 021-51666838

Xiaodan Yu 021-20707870

Rui Ma 021-51595780

Disheng Feng 021-51666714

Yujun Liu 021-20707895

Yanlin Lü 021-20707875

Zhicheng Zhou 021-51666711

Haohan Zhang 021-51666752

Zihan Wang 021-51666914

Xiaoxuan Ren 021-20707866

Jie Wang 021-51595902

Yang Xu 021-51666760

Boling Chen 021-51666836

![[SMM PV News] RayGen Deploys 1 MW Solar and Thermal Storage System in Brazil](https://imgqn.smm.cn/usercenter/QGlKw20251217171730.jpg)

![[SMM PV News] Middle East 'LNG' Strikes Impact PPA and BESS Economics](https://imgqn.smm.cn/usercenter/oVqJl20251217171730.jpg)

![[SMM Analysis] Why 2026 is the Definitive Year for Long-Duration Energy Storage](https://imgqn.smm.cn/usercenter/WyqWW20251217171729.jpg)